Worried About Impacting Your Credit Score?

by Jon Mohatt (aka Travel Brainstorm)

If you have read my recent posts you know that I have just retired from the Air Force and moved my family to Montana where we are in the process of building our retirement home. With this new home comes a new mortgage where we will want to minimize our interest rate by ensuring our credit rating is as strong as possible. Generally speaking, a score of 760 or higher will put one in the running for the best rates, but I like to shoot for even higher so that the application process is quick and easy with minimal worries from the underwriters.

By reading my past posts you also know that the quickest method to accumulate lots of reward points is through acquiring bonuses from applying for new travel related credit cards which I love to do as its literally free money, if done right. Many people refer to this process as credit card “churning”, but that is a dated and inaccurate term as most credit card companies no longer allow you to churn their credit cards one after another just to get the sign on bonuses multiple times. Some folks like to perform app-o-rama’s which involves applying for multiple credit cards at the same time to minimize hard credit bureau pulls while maximizing applications for the most lucrative offers at the same time.

Needless to say, if done wrong, churning and app-o-rama’s can have a negative impact on your credit score and you don’t want to be negatively impacting your credit score before applying for a mortgage. Check out my post on how to do app-o-rama’s right. Using credit cards is the one Dave Ramsey rule that I don’t like and don’t follow. Many say one should be skeptical of applying for multiple credit cards right before a large purchase and say to not apply for new credit 18-24 months before you plan to apply for a loan. I certainly agree that one should be extra cautions right before a large purchase where you will be applying for financing, but feel 24 months is a bit excessive. In order to prove this point and to calm people’s fear of applying for multiple credit cards in general I will show how I have managed to maintain an excellent credit score while applying for five credit cards 13 months before applying for a mortgage. Remember, it has to be done right! When done right, impacting your credit score, shouldn’t be a major concern.

In a recent article I read on the Fox Business web site (www.foxbusiness.com) they noted six must-dos before purchasing a house. These six actions are

1 – Strengthen your credit score

2 – Figure out how much house you can afford

3 – Save for down payment and closing costs

4 – Build a healthy savings account

5 – Get preapproved for a mortgage

6 – Buy a house you like

Of course, first and foremost is strengthening one’s credit score and that was exactly what we have been doing, but it didn’t stop me from applying for five new travel reward credit cards in October 2013. The sign on bonuses from this app-o-rama provided 285,000 reward points and a Southwest Airlines Companion Pass, one of the greatest travel perks in the business. Many of these points, along with the Southwest Airlines Companion Pass is what made our $66 Key West vacation a reality!

Now, remember, I have always had good credit so I cannot make any guarantees as to the impact on your credit score if you were to apply for multiple credit cards 13 months before applying for a mortgage. I have a very long and blemish free credit history that I am sure helps keep my score high. I am just showing that if you too follow the rules I have laid out in the past and have maintain your credit history as I have, it should be OK to maintain your app-o-rama’s right up to 12-18 months before applying for a large loan without it noticeably impacting your credit score.

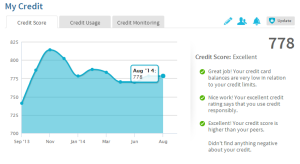

Below is the impact to my credit score based on results from Credit Sesame, Credit Karma and Barclaycard’s FICO score tool.

Credit Sesame History

Credit Sesame (from 740 back up to 778)

Credit Karma History

Credit Karma (from 765 back up to 780)

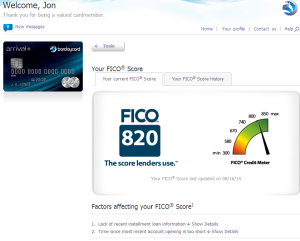

Barclaycard FICO Score Tool

Barclaycard FICO Score Tool (from 816 back up to 820)

The factors listed as impacting my FICO score were #1 “Lack of recent installment loan information” and #2 “Time since most recent account opening is too short”. Isn’t it funny and/or ironic that #1 is because I am completely debt free and should actually improve my credit worthiness and #2 is the very focus of this blog post?

As one can clearly see, my credit score took a slight dip after my latest app-o-rama in October ’13, but then bounced right back and went even higher after only 10 months, but I certainly do not plan to apply for any more credit cards until after our mortgage is finalized in November. My wife and I have already been pre-approved for our mortgage and cant wait to move into our new home and begin planning for our next adventurous trip!

As always, happy brainstorming and safe travels! Be sure to sign up to be notified of future blogs posts (top of right sidebar), let your friends know about this blog and “Like” the Travel Brainstorm Facebook page! I also have many reviews on TripAdvisor, just search for “TravelBrainstorm”!

![]()

I just saw where JD Powers have released their latest credit card satisfaction survey. You can review the results on their web site at

http://www.jdpower.com/press-releases/2014-us-credit-card-satisfaction-study